The circular carbon economy seeks to capture and use CO2 emissions in an economically viable and environmentally friendly cycle. In this paradigm, CO2 is a carbon feedstock that is recycled into valuable products rather than becoming environmentally hazardous waste.

The chemistry of CO2 is fundamental to the development of a commercially viable circular carbon economy. However, for this to happen, molecular CO2 needs to be captured from ambient air and point sources through adsorption and desorption processes before it can be converted into useful products, such as commodity chemicals and fuels, construction materials, and plastics. These capture and conversion processes are already being explored or put to use, facilitated by pivotal technologies built to help set up a circular carbon economy.

This circular carbon economy, a vital tool for mitigating climate change, is still in its infancy, and its realization will require innovative capture and utilization processes. The laboratory chemistry underpinning such processes has to be creatively engineered, scaled, and piloted to demonstrate technical and economic feasibility, providing the information needed for an initial assessment of the commercial viability.

The Circular Carbon Market Report

Insight into its commercial growth is available from the 2022 Circular Carbon Market Report published by the Circular Carbon Network, an XPrize initiative. It documents trends in the overall growth of the sector and its components, including the number of firms, their level of technological readiness, revenue and investment, as well as uses of the captured CO2.

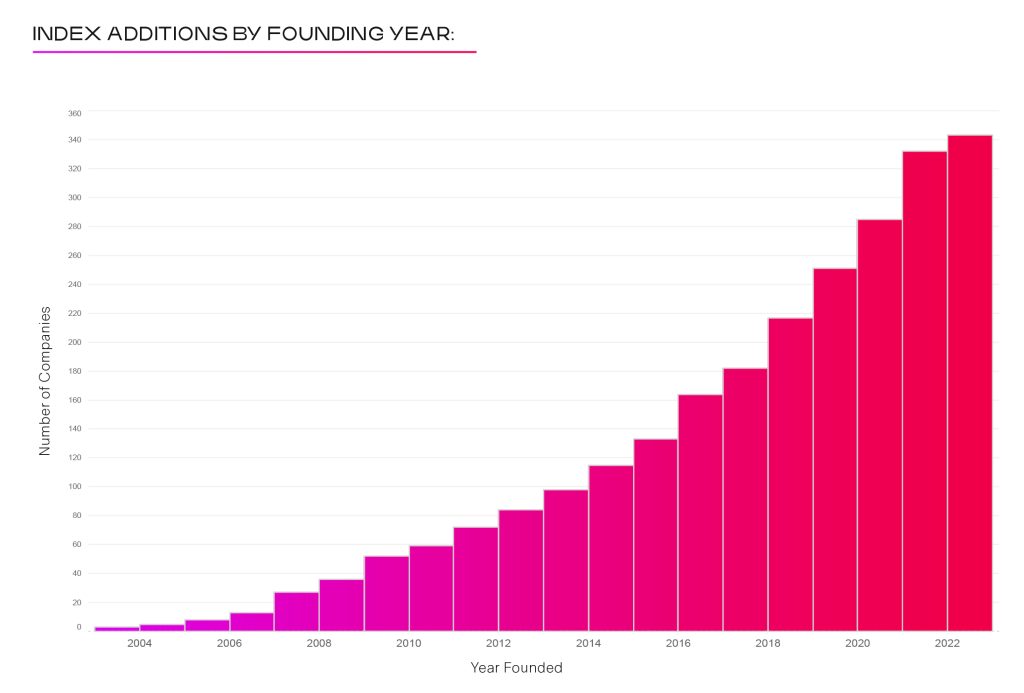

Over the past two decades, the carbon market has grown exponentially, currently adding over 300 companies per year, meaning that about 26% have been established in the past three years alone. Close to 700 companies in 55 countries displayed by activity and scale in the world map have attained the pilot phase of their projects, operating or in progress, with reported seed or pre-seed capital raised of $5.77B. Activity is roughly equally distributed between three global blocks: North and South America, Europe, and Asia.

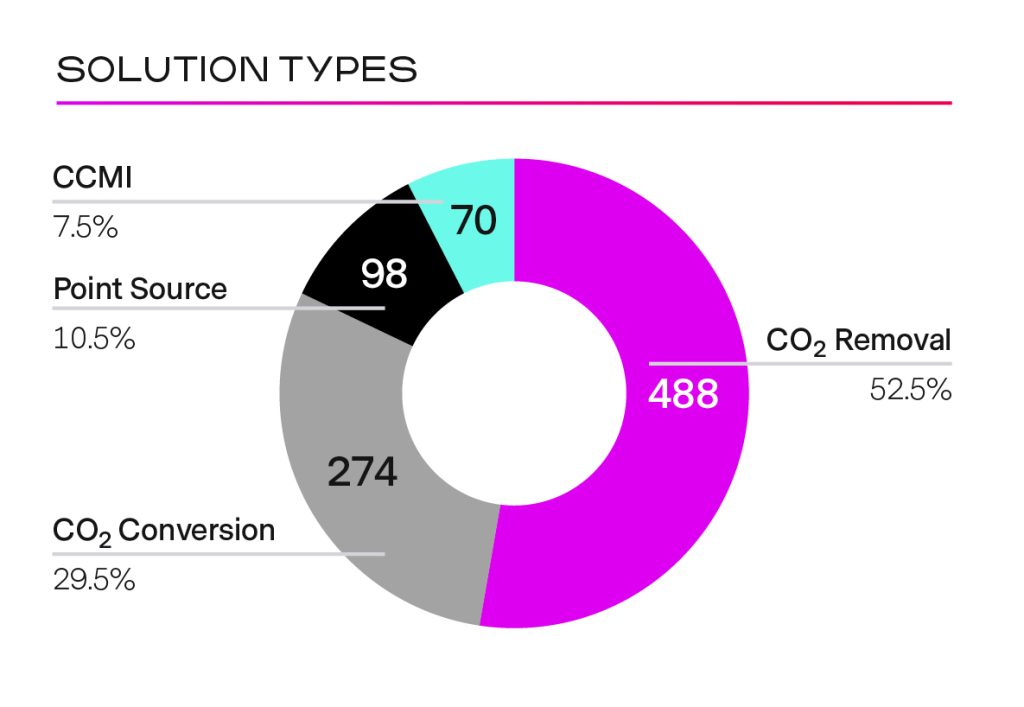

Over 60% of the companies focus on CO2 capture, with 10.5% capturing CO2 from point sources and 52.5% from ambient air. Almost 30% target CO2 conversion and the balance provide circular carbon market infrastructure (CCMI) services, such as project development and verification.

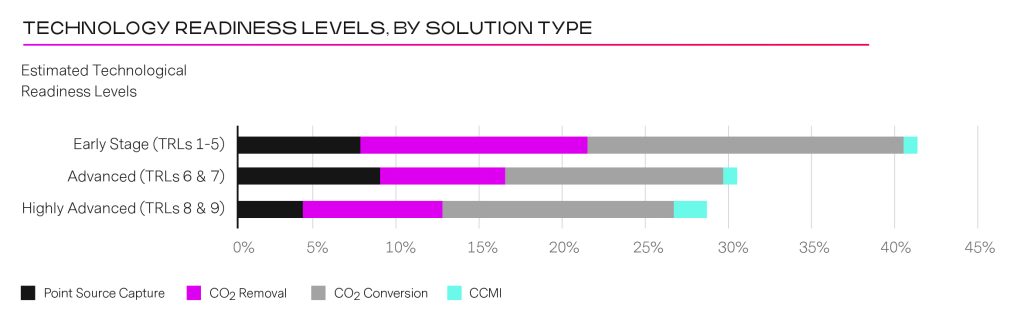

The sector is still relatively young, and as such, only about 40% of the processes under development have reached a technological readiness level (TRL) of 1 to 5. Of the remaining processes, about half (31%) have reached a TRL of 6-7, and the other half (28%) are highly advanced with a TRL of 8-9. Overall, this reflects the rapid growth and development of the circular carbon economy.

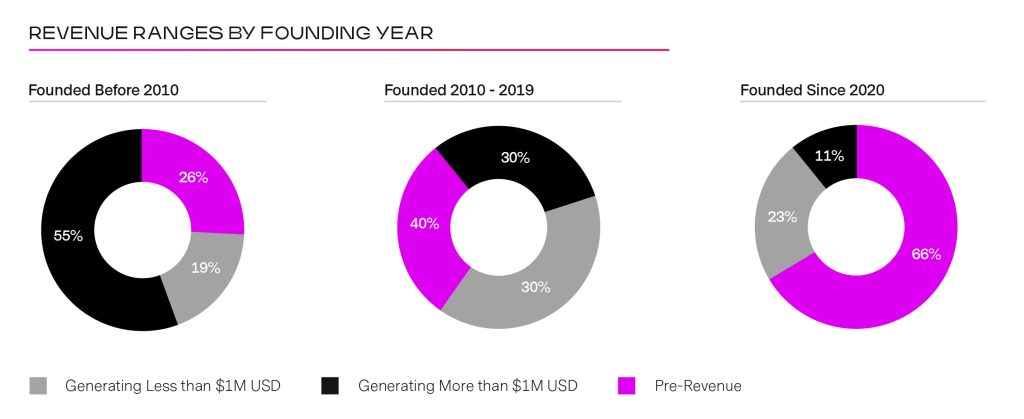

The circular carbon economy sector is estimated to generate annual revenues ranging between $0.97B to $2.46B. Most of the revenue in the sector is currently being generated by established companies. Of the companies founded before 2010, 26% have managed to survive without generating revenue yet. Despite this, investors remain optimistic about the potential of their technologies and continue to fund development for more than a decade. Of the companies founded since 2020, 66% are not yet generating revenue, while 34% have some commercial activity already.

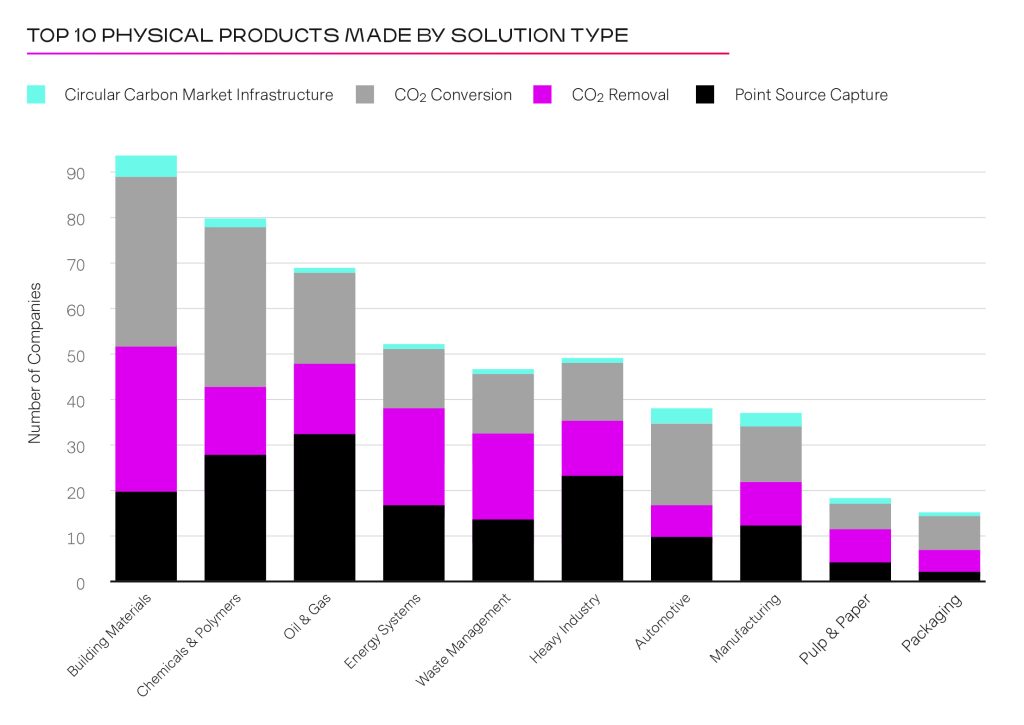

The markets for these processes are diverse. Based on data for the companies manufacturing the top ten products by solution type, the largest markets are companies in building materials, chemicals and polymers, and oil and gas industries. Other applications are in the energy systems, waste management, heavy industry, automotive, manufacturing industries, with smaller contributions from pulp and paper, and packaging firms. In all cases they use combinations of point source and ambient air capture and conversion processes.

The development of the circular carbon market is supported by more than 100 organizations, ranging from non-profit advocacy to industry associations. These organizations provide essential infrastructure support and direction to help the growing number of companies access the necessary services, expertise, resources, and support to help them survive and flourish.

The performance metrics collected by the Circular Carbon Network provide an encouraging overview of the sector’s strength and vibrant growth, offering reasons for optimism that the circular carbon economy is a realistic vision for achieving a sustainable and safe future.

Written by: Geoffrey Ozin, Solar Fuels Group, University of Toronto, www.solarfuels.utoronto.ca, and Erik Haites, Margaree Consultants, Toronto, www.margaree.ca

Figures and images courtesy of XPRIZE